Anchorage Digital, a federally chartered cryptocurrency bank and stablecoin infrastructure provider, has submitted a public comment letter supporting the U.S. Department of the Treasury’s proposed anti-money laundering (AML) and sanctions framework for the GENIUS Act, arguing that the rules largely strike the right balance between compliance and innovation.

In a letter published Wednesday, Anchorage said the proposed framework appropriately imposes AML obligations on regulated stablecoin issuers, while adjusting Treasury to clarify responsibility for secondary market sanctions, enterprise-wide AML programs, and correspondent account requirements.

Specifically, Anchorage argued that issuers should not face strict liability for failing to independently identify sanctioned users transacting in secondary markets through their smart contracts.

“A final rule that is clear and actionable provides regulated institutions with the certainty they need to build and strengthens U.S. leadership in the next generation of payments and settlement infrastructure,” Anchorage said.

Fountain: Kevin Wysocki

The comments address Treasury rules proposed in April that would classify payment stablecoin issuers as financial institutions under the Bank Secrecy Act, subjecting them to anti-money laundering, customer due diligence and suspicious activity reporting requirements.

The proposal, issued jointly by the Financial Crimes Enforcement Network (FinCEN) and the Treasury’s Office of Foreign Assets Control (OFAC), would align stablecoin issuers with existing US anti-money laundering and sanctions compliance standards, while imposing enhanced monitoring and record-keeping obligations.

Related: Solana Institute CEO Says CLARITY Act Should Protect Open Source Developers

Industry groups push for broader sanctions exemptions

Support for the proposed regulation has not been uniform across the crypto industry.

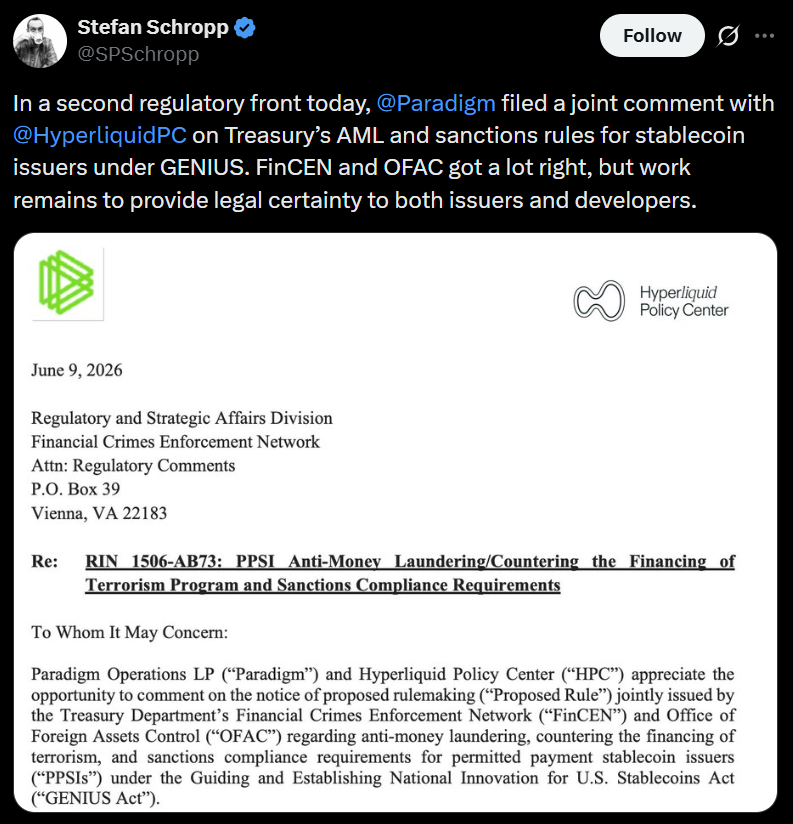

Lobbyists from crypto derivatives exchange Hyperliquid and venture capital firm Paradigm recently submitted their own comment letter seeking greater clarity on secondary market obligations, echoing Anchorage’s concerns but taking a more critical view of the proposal overall.

Fountain: Stefan Schropp

The groups argued that the current framework could impose sanctions obligations on issuers even when they lack a direct relationship or visibility to users transacting in secondary markets.

“OFAC includes secondary market activity in the issuer’s enforcement perimeter, treating smart contract interactions as an ongoing ‘provision of services’ that carries sanctions, regardless of whether the issuer has any relationship or visibility with the parties to the transaction,” they said.

Related: SEC’s Peirce Republishes DeFi Code Is Protected Speech